Want to download the Market View - Autumn Edition as a PDF? - click here.

As the UK’s largest recruiter, Staffline is particularly well placed to provide commentary on industry and government reports published on the recruitment industry. We combine the information available in these reports with insight from Staffline’s team of more than 650 recruiters around the nation - drawing upon the trends we see emerging in our 1.6 million-strong worker database and from our customer base of close to 1,000 businesses and brands.

In this Autumn edition of the Market View, we examine optimal ways of working that will enable our customers to meet the macro-economic challenges at play in the current market and also take a look at what we see coming down the track in terms of the outlook for specific sectors.

2023 - Testing Times

Supply chain challenges and the bite of inflationary pressures continue to impact consumers and businesses alike.. Business closures are up, cost of living is up and the pound in your pocket buys you less each day.

The wheel always turns however, and UK PLC is showing some early signs of resilience by quickly aligning with the new reality and fighting back. Many market-leading businesses are seeing this as an opportunity to increase market share by discounting to support the customer, whilst minimising fixed overheads, outsourcing ‘non-core’ activities, simplifying product ranges and service lines and aligning costs as closely as possible to a volatile market.

Times are tight and ‘agility’ is the watchword.

The agile and flexible business that is completely aligned to client demand can still perform well, even in a difficult market, and can certainly ensure that it is positioned to take maximum advantage when consumer confidence and spending returns.

Every cloud has a silver lining and one of these is a re-balancing of the labour market away from a candidate-dominated landscape to a more even level. More available candidates competing for fewer roles means that companies can raise expectations and drive productivity and performance, maximising the return and cost effectiveness of their people resource.

What about peak?

With Autumn comes the run into Christmas, Black Friday and all that jazz. While we hesitate to use the phrase ‘green shoots’, the early signs are that this year’s peak looks like it will more closely resemble peak-periods from before the COVID-19 pandemic.

Of course, predicting anything for definite at the moment is tricky, but we have definitely seen some stronger demand in September into October. However, what does seem increasingly unlikely is a smooth ramp and increase in the demand curve.

Expect spikes, nothing then everything, surprising product successes that drive up demand and - likely as not, a few unfathomable flops that do little to encourage an upswing.

Inflation's Ongoing Impact

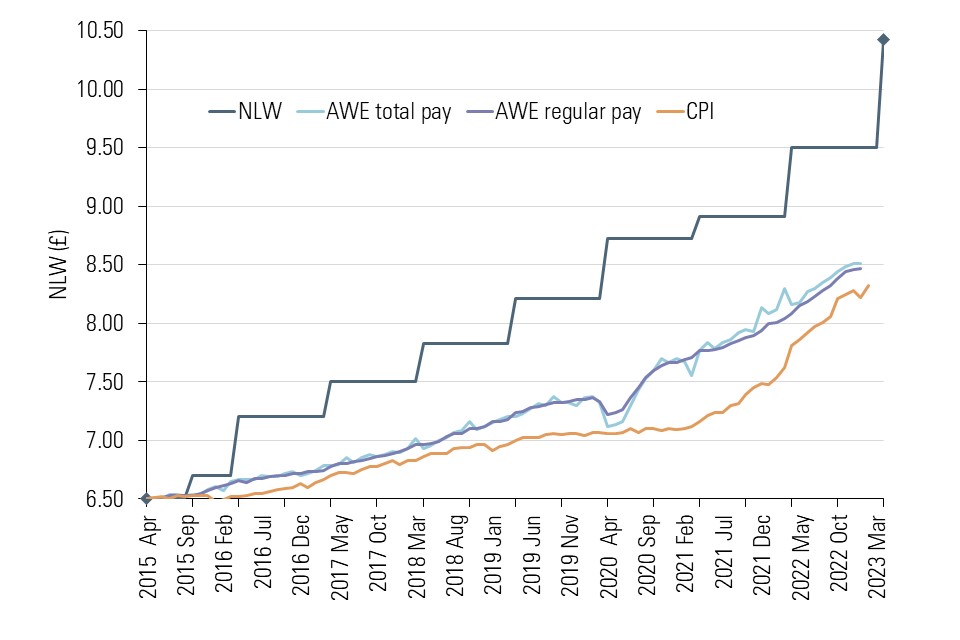

Wage inflation at 5% is lagging significantly behind food inflation at 14.9%.

Whilst food and general inflation is easing, wage inflation will continue to rise. This is especially critical in lower paid sectors such as food manufacturing that are heavily impacted by living wage increases.

This year saw the highest ever National Living Wage increase at 9.7%, with 2024 likely to see another significant rise. The latest government statement is for a rise to ‘at least £11:00’, with previous statistics suggesting an increase to around the £11.16 level, which will be a further 7.1% increase. This will not just affect entry level roles, as companies will be under pressure from individual employees and unions to maintain shift and skill differentials for higher paid positions.

Source: The National Minimum Wage in 2023 - GOV.uk

Interest rates and general inflation will also remain higher than recent years, meaning that consumers will continue to have less disposable income in their pockets. This means ongoing demand reduction leading to a likely overall recessionary (in real terms) environment for the foreseeable future.

Market 'Winners' & 'Losers'

A combination of broader macro trends - think environmental, geopolitical and global-national financial constraints, combined with more localised events (including the influence of social media), will continue to increase the need for flexibility amidst ongoing market uncertainties.

A global financial tightening will likely increase cross-border competition, potential tariffs and embargoes.

This may well call out weaknesses in globalised supply chains, as will consumption increases (driven by population rise). Negative weather incidents are also on the rise, threatening harvests and supply of raw materials in a manner that continues to be unpredictable. When this is paired with demand trends driven by social media ‘hot products’ and celebrity endorsements, minimisation of fixed costs and flexibility of workforce will be critical for success.

Candidate Availability On the Rise

According to a recent report, 19% of UK employers indicated that they are planning to make redundancies in Q1 2024.

Alongside this, data shows that insolvencies in the food & drink sectors rose by more than 100% in 2023 (year-to-date) versus the same period just 12 months earlier.

All this points to a more difficult economic environment. And, as more businesses fail outright, others will cut costs (including those associated with their workforce) to ensure they survive. As a result of more lay-offs and business closure, more labour and candidates will become available than has been the case in recent years, particularly at lower skill levels.

Staffline has seen a steady increase in labour availability in 2023 and expects this trend to continue medium-term.

More competition for jobs means that employers can afford to be more picky in their hiring and can revise views on elements such as paying parity with legacy employees from day one. Furthermore, there can be a more proactive management of worker performance as there will be more available candidates if employees are unable or unwilling to achieve performance targets.

This is a definite turn to an employer market rather than a candidate market for high-volume, lower skilled roles. Skilled and hard-to-fill roles will remain hard-to-fill in the short-to-medium term, however a general market downturn will begin to affect the entire employment market over time, especially in the case of business failures where all employees will be in the same boat.

Business & Recruitment Process Outsourcing (BPO/RPO)

Market volatility and uncertainty is driving increased business outsourcing of recruitment activity, both in terms of flexible and permanent hiring as companies quickly try to realign fixed costs in a variable market.

The last two years had seen rises in perm hires and ‘insourcing’ in order to retain labour in a candidate-led market. Now, this strategy is reversing quickly as companies look at ways to outsource as much cost as possible, including payroll, talent attraction and even entire workforces.

Outsourcing is a long-term business trend that was put into hiatus over the COVID-19 period and the recent labour shortage years, but is now returning apace.

Companies are reviewing exactly how much fixed cost they need for minimum trading expectations and how to increase flexibility. We are speaking with more and more with companies about moving away from expensive legacy practices, increasing their flexible workforce percentage and outsourcing permanent talent acquisition for all frontline roles.

The aim is to flexibly align workforce hiring and costs exactly with market demand and pay rates.

The Pipeline of Labour

In line with the overall market outlook, as businesses continue to struggle or fail and as redundancies rise on the back of this, we increasingly we expect to see UK labour needs to be met from within the existing ‘domestic’ pool of labour. And, as noted previously, at Staffline we’ve already started to see significant increase in candidate and worker availability coming through.

Despite the expected impact of Brexit, net ‘long-term’ immigration into the UK in 2022 was 606,000.

This compares to 206,000 in 2005, 256,000 in 2010, 329,000 in 2015 and 488,000 in 2021. The overall number of non-EU students is falling with humanitarian immigrants (e.g. Ukrainian nationals) rising.

It is extremely difficult to predict future trends and whether humanitarian immigrants will remain in the UK or return, however there is still a strong flow of net migration into the UK which will continue to grow the workforce for lower skilled roles.

There are also opportunities to access new pools of labour due to government incentives and funding including the Youth Mobility Scheme and British Overseas Citizen scheme, as well as ESG and funding benefits from social recruitment.

Watch Out: New Legislation May Impact Your Workforce!

There are 2.1m EU nationals in the UK whose applications for settled status are currently under review. Previously, even if the applications were rejected, individuals could reapply and stay and work in the UK. From 9th August repeat applications are not allowed, so these 2.1m people may need to leave the UK within 2 weeks if their application is rejected. When the rejections will occur will depend on the government processing time, but some rejection letters have already been issued.

Many of these individuals are working in frontline roles. If the government does not change policy there is potentially significant compliance issues for illegal working and/or impact of having to replace EU nationals with newly available UK registered workers. Are you monitoring this situation with your own employees?

ESG - A Spotlight on Social Recruitment

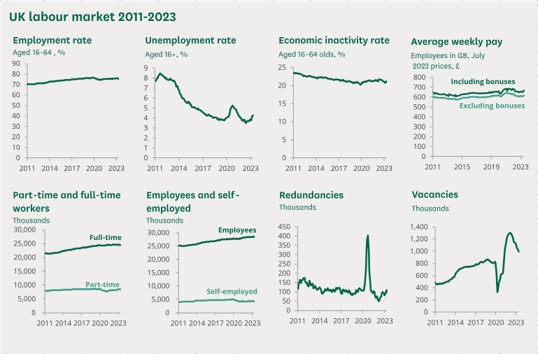

Latest ONS figures show that unemployment rose in July from 4.2% to 4.3%. 1.46m people over the age of 16 are unemployed. This is a significant recent uptick that looks set to continue for the foreseeable future.

Source: Labour Market Outlook: Summer 2023 - CIPD

There are 8 million people between the ages of 16-65 who are ‘economically inactive’. UK government provides £2.7 billion annual funding for employment and skills, focused on helping the economically inactive and under-represented populations into the workforce. There are 27 identified demographics that attract funding from carers coming back to work through to ex-offenders and BAME applicants.

The Opportunities:

1. Fully-funded pre-employment training tailored to individual client need with a wide range of industry specific qualifications attached.

2. A new pipeline of workers with strong loyalty.

3. Making a social impact with a clear calculation of social benefit. Average c£21,000 per head recruited through the Group’s Social Recruitment Framework.

4. Maximisation of Apprenticeship levy and in-work learning utilising the Adult Education Budget.

5. Contribution towards achievement of ESG targets.

Our PeoplePlus Group company gives Staffline and our clients a clear market advantage in this area, with a seamless pipeline of Social Recruitment candidates and funded training opportunities.

PeoplePlus has helped 1 million disadvantaged people into training and employment since 2018.

Further Reading & Sources

Sources and useful links:

Market View: Spring Edition - Staffline

Labour Market Outlook: Summer 2023 - CIPD

Surge In Insolvencies Amongst Food and Drink Manufacturers - KamCity

Youth Mobility Scheme Visa: Overview - GOV.UK

Long-Term International Migration, Provisional - ONS

Get in Touch

If you've got any questions or comments regarding the content, please contact James Wilson (Chief Sales Officer at Staffline) on: james.wilson@staffline.co.uk or a member of the New Business Team on: newbusiness@staffline.co.uk.

Editor's Notes

James Wilson, Chief Sales Officer at Staffline, has worked in the flexible recruitment industry for 25 years in operational and business development roles, including 15 years with Staffline.

During this time, he has developed many high value relationships, helping UK businesses maximise opportunities from their recruitment supply chain, and building temporary and permanent recruitment services solutions on a national basis.

Staffline Group PLC is the UK and Ireland’s largest recruiter and social employability business, supplying 50 million flexible workforce hours and 7,000 perm placements annually to many leading brands from 450 locations.

An Overview of Staffline

Founded in 1986, Staffline is the UK’s leading provider of flexible blue-collar workers, supplying approximately 50,000 staff per day on average to around 450 client sites, across a wide range of industries including agriculture, supermarkets, drinks, driving, food processing, logistics and manufacturing.

Find out more at: https://www.staffline.co.uk/